Why Are Digital Signatures Becoming a Strategic Priority for MFIs Worldwide?

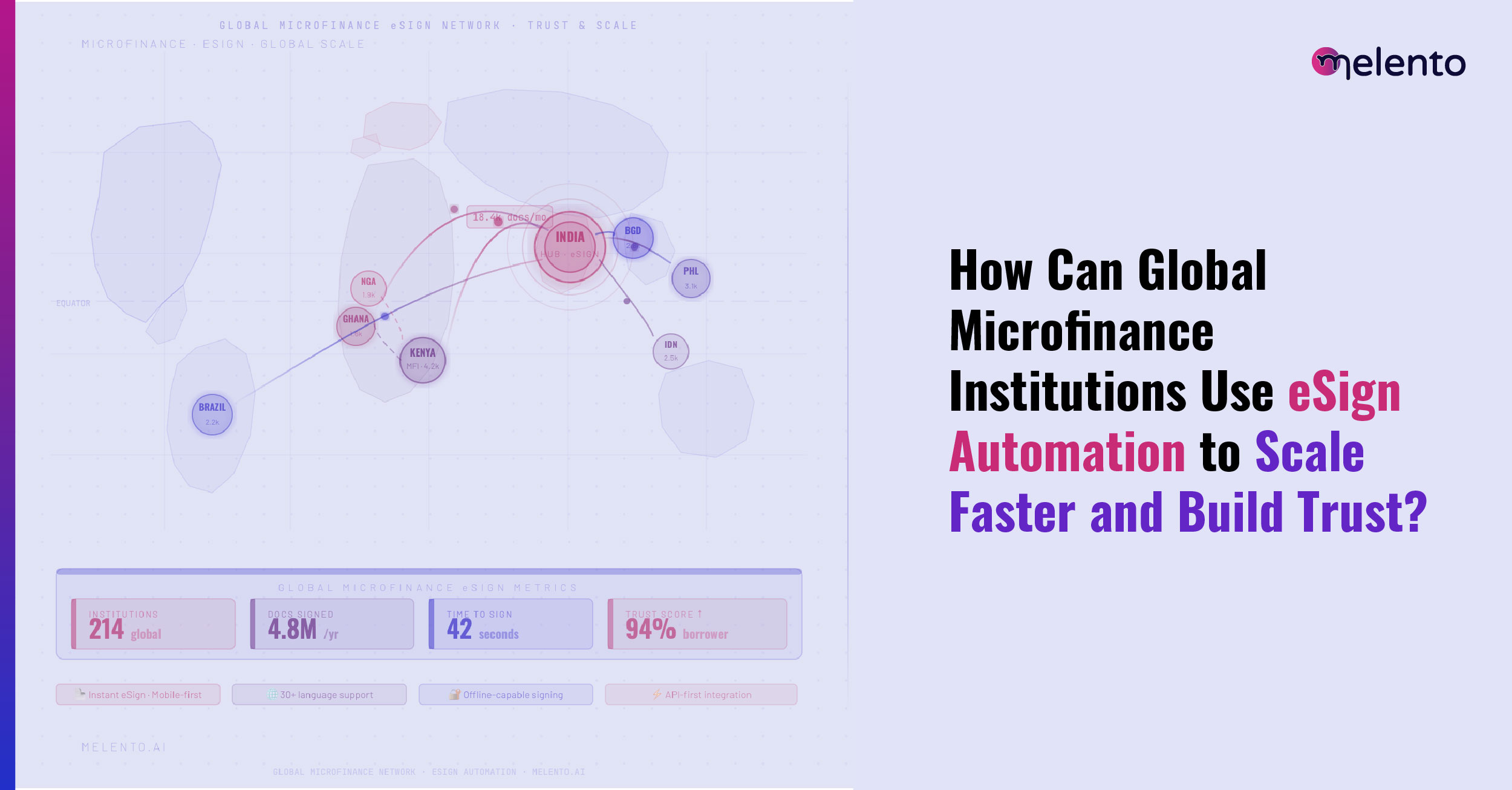

Microfinance is evolving rapidly across global markets. For lenders operating across regulated markets, the ability to onboard, verify, authenticate, and execute agreements digitally is becoming a baseline expectation. From Southeast Asia and Latin America to Africa and the Middle East, financial inclusion is increasingly being powered by digital lending infrastructure.

According to the World Bank, nearly 1.4 billion adults globally remain unbanked, yet over two-thirds of them now own mobile phones. This creates a significant opportunity for microfinance institutions (MFIs) to reach underserved borrowers digitally.

At the same time, McKinsey estimates that digital finance could add $3.7 trillion to emerging-market GDP by 2025 by expanding financial access and improving efficiency.

This shift is also being reinforced by legal and regulatory frameworks across global markets that increasingly recognize digital signatures as legally valid and commercially enforceable.

Several major regions have already established strong digital signature legislation, including:

- The European Union eIDAS Regulation, which standardizes electronic signatures across member states

- The United States Congress ESIGN Act, enabling legally binding electronic signatures across U.S. commerce

- India’s Information Technology Act, 2000, which provides legal recognition to digital signatures and Aadhaar-authenticated eSign workflows

- The United Nations Commission on International Trade Law Model Law on Electronic Signatures, adopted as a framework by multiple countries

- Digital transaction laws across markets like the United Arab Emirates, Kenya, and Brazil, all of which increasingly support legally enforceable electronic execution

This global regulatory momentum signals a clear reality: Digital signatures are now essential financial infrastructure.

As Ajay Banga, former CEO of Mastercard and current President of the World Bank, observed:

“Digital public infrastructure is one of the most powerful accelerators of financial inclusion.”

For MFIs, digital signatures are a critical part of that infrastructure.

What Challenges Are MFIs Facing in High-Velocity Lending Markets?

The pressure to deliver faster, more accessible credit is growing globally.

Borrowers now expect:

- Instant onboarding

- Mobile-first experiences

- Minimal paperwork

- Faster disbursement

However, many MFIs continue to struggle with fragmented execution systems.

Common issues include:

Problem:Borrower Drop-Off During Agreement Execution

A report found that friction in digital onboarding processes can increase abandonment rates by 30-50%, particularly during identity verification and authorization stages.

When digital signature workflows are slow, unclear, or unreliable, borrowers disengage.

Problem: Operational Bottlenecks

Manual intervention in signature workflows often creates delays. Examples include:

- Failed OTP authentication

- Document version mismatches

- Delayed approvals

- Manual audit reconciliation

In competitive lending environments, these delays directly impact conversion rates.

Problem: Compliance Complexity Across Markets

Different geographies impose different regulatory requirements. Examples include:

- eIDAS in Europe

- ESIGN Act and UETA in the United States

- Digital identity regulations across MENA and LATAM

- Aadhaar-linked authentication frameworks in India

For global or multi-market lenders, maintaining compliance across these frameworks is complex without integrated digital signing systems.

Why Is Compliance Alone No Longer Enough?

Historically, MFIs adopted eSign to satisfy regulatory requirements. Today, that baseline is insufficient. Digital signature infrastructure now influences:

- Borrower acquisition

- Customer retention

- Loan turnaround time

- Operational scalability

- Brand trust

For modern financial institutions, this translates into a simple truth:

- Every lender is now a digital experience company.

- Compliance may keep institutions operational.

- Experience is what makes them competitive.

How Can MFIs Turn Digital Signatures into a Competitive Advantage?

The answer lies in repositioning digital signatures from compliance tools to growth infrastructure.

Forward-thinking MFIs use eSign to optimize:

- Borrower Experience: A seamless signing process increases trust and completion rates.

- Operational Efficiency: Automation removes manual dependencies.

- Scalability: Systems can handle larger volumes of borrowers without proportional increases in staffing.

- Regulatory Readiness: Compliance becomes embedded in workflows rather than being enforced manually.

As per studies, organizations implementing workflow automation and digital process orchestration can reduce operational costs by up to 54% while significantly improving customer response times.

For MFIs, these gains directly impact profitability and reach.

Why Is Reliability More Important Than Speed?

Speed attracts borrowers. Reliability retains them. A fast but inconsistent signing process creates friction and distrust. A dependable process builds confidence.

This is especially important in microfinance, where many borrowers are:

- First-time digital finance users

- Located in low-connectivity environments

- Highly sensitive to process complexity

Reliable digital signatures strengthen that trust.

What Does Digital Signature Failure Cost Financial Institutions?

The costs are often underestimated. When digital signature systems fail, institutions face:

- Lost Revenue: Borrowers abandon incomplete applications.

- Higher Operational Costs: Support teams intervene manually.

- Compliance Exposure: Missing audit trails create regulatory risk.

- Brand Erosion: Borrowers lose confidence in the lending process.

An insights survey found that 32% of customers stop engaging with brands after just one poor digital experience. In lending, that number can translate directly into lost business.

What Is the Solution for MFIs Looking to Scale Globally?

MFIs need digital signing infrastructure built for scale, reliability, and regulatory adaptability. This means adopting platforms that combine:

- Legally compliant digital signatures

- AI-powered identity validation

- Workflow orchestration

- Real-time auditability

- High-volume transaction resilience

This is where Melento eSign delivers strategic value.

How Does Melento eSign Help MFIs Move Beyond Compliance?

Melento transforms digital signatures into an intelligent workflow infrastructure. Rather than treating signing as a standalone event, Melento embeds it within end-to-end lending execution.

Problem: Fragmented Signing Journeys

Solution: Workflow-Integrated eSign

Melento integrates document generation, signing, approvals, and disbursement readiness into a single automated flow.

Problem: Verification Errors

Solution: AI-Powered KYC

Melento’s AI-driven KYC validation detects inconsistencies, flags anomalies, and reduces manual review effort. This improves both speed and accuracy.

Problem: Regional Compliance Complexity

Solution: Flexible Compliance-Ready Architecture

Melento supports digital identity and signature workflows adaptable across regulated lending environments. This enables institutions to operate confidently across markets.

Problem: Limited Visibility

Solution: Real-Time Audit Trails. Every action is logged through:

- Timestamping

- Consent capture

- Authentication records

- Document traceability

Problem: Scaling Constraints

Solution: High-Volume Reliability

Melento is designed to support institutions that process thousands of agreements without degrading workflows.

What Business Outcomes Can MFIs Expect with Melento eSign?

Institutions implementing intelligent digital signing typically achieve:

- Faster Agreement Execution: Reduced turnaround from hours or days to minutes.

- Lower Borrower Abandonment: Frictionless execution improves completion.

- Improved Operational Productivity: Automation reduces repetitive manual work.

- Stronger Compliance Readiness: Audit trails are built-in.

- Scalable Growth: Operational capacity increases without an equivalent increase in staffing.

Why Will Digital Signature Strategy Define the Future of Microfinance?

The next generation of MFIs will compete not just on credit access, but on execution quality. Borrowers will increasingly choose institutions that offer:

- Seamless onboarding

- Instant authentication

- Transparent agreements

- Reliable digital journeys

Digital signatures influence all four. They are no longer a compliance checkbox. They are a competitive lever.

What Should Forward-Thinking MFIs Do Next?

MFIs should evaluate whether their current digital signature infrastructure supports growth.

Ask:

- Are borrowers abandoning at the signing stage?

- Are workflows dependent on manual intervention?

- Are audit trails complete and automated?

- Can systems scale globally?

If not, there is a strategic opportunity. Platforms like Melento eSign, with workflow intelligence, help institutions transform digital signatures into a true competitive advantage. How?

- Fraud-Proof Signing Workflows: Use AI to combine identity checks, live image capture, GPS tagging, and signature match to create highly secure signing journeys that reduce fraudulent loan applications.

- Mobile-First Signing Experience: Enables borrowers in remote regions to complete agreements seamlessly, critical for financial inclusion across emerging markets.

- Bulk Digital Agreement Signing: Allows MFIs to process high volumes of loan contracts simultaneously, improving efficiency for large-scale lending programs.

- Multilingual Borrower Signing Journeys: Supports region-specific language interfaces, helping borrowers clearly understand terms and improving trust across diverse borrower populations.

- End-to-End Audit Trails: Maintains complete timestamped records of borrower authentication, approvals, location data, and signing activity, strengthening compliance and dispute resolution globally.

- WhatsApp Integration: Stay informed in real time with WhatsApp notifications, signing links, OTPs, completed documents, and audit trail reports.

Because in global microfinance, access gets borrowers in the door and trust keeps them there.